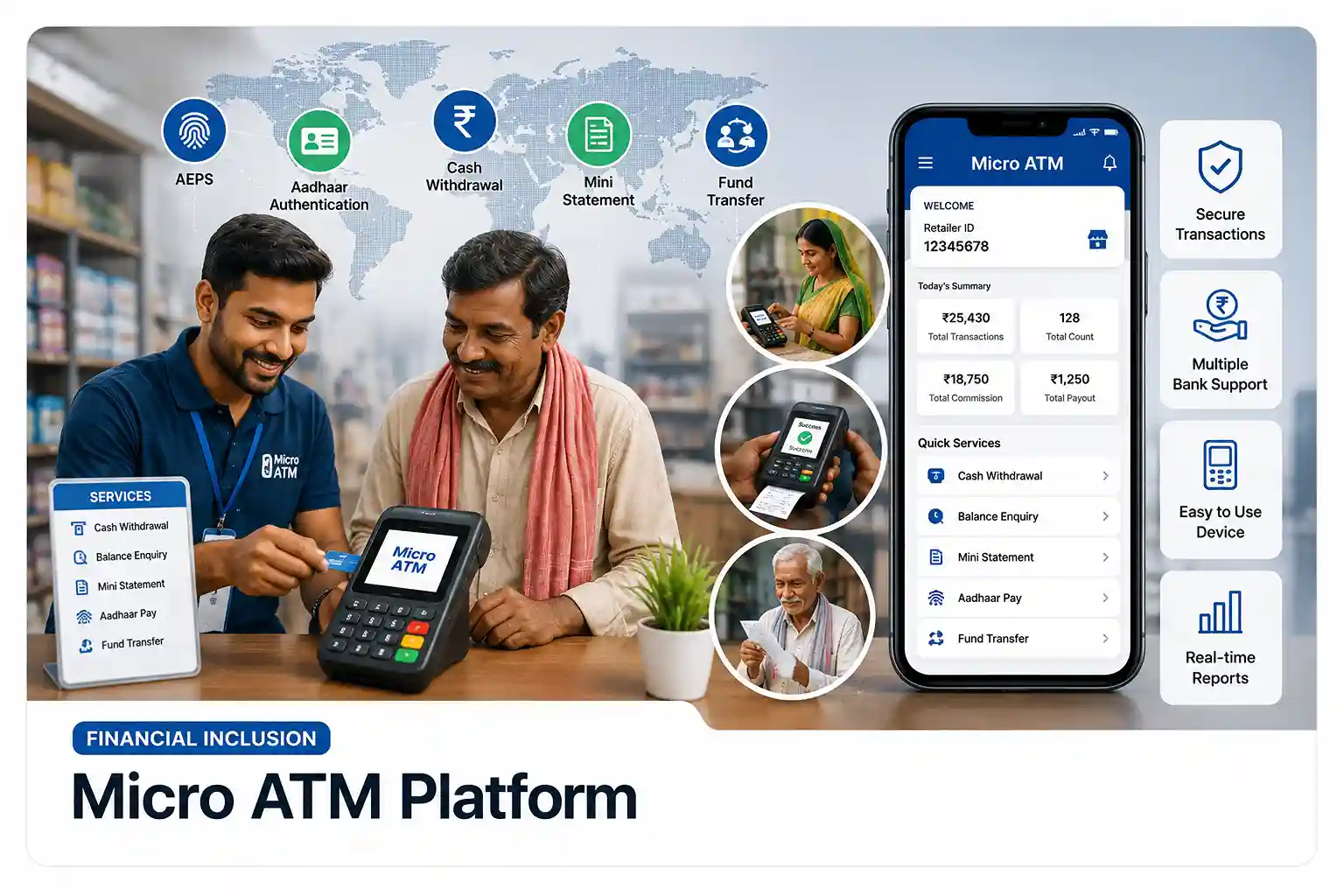

Top Features Every Successful Micro ATM Platform Must Have

Digital banking has changed how customers access financial services, especially in areas where

traditional banking infrastructure may not be easily available. Micro ATM

technology allows banking services to reach customers through retailers and agents

using compact devices that support secure financial transactions. These systems play an

important role in extending banking accessibility while reducing dependency on physical bank

branches.

A modern Micro ATM platform should provide much more than simple cash

withdrawals. Users expect balance enquiries, mini statements, instant transaction processing,

payment confirmations, and secure authentication systems. Businesses operating banking

ecosystems also require retailer management modules, commission systems, transaction dashboards,

analytics tools, and scalable banking integrations.

Modern fintech ecosystems frequently integrate Micro ATM solutions with AEPS

Banking systems, Money Transfer platforms, UPI QR Payment systems, and BBPS services.

Combining multiple banking and payment services creates stronger customer engagement and expands

business opportunities.

If you are planning to build a digital banking ecosystem, below are the key features every

successful Micro ATM platform should include.

1. Cash Withdrawal Integration

Cash Withdrawal Integration refers to a feature in digital payment systems that allows users to withdraw cash directly from their bank account or digital wallet using authorized channels such as UPI-enabled ATMs, micro-ATMs, or merchant point-of-sale (POS) devices. In a UPI-based ecosystem governed by the National Payments Corporation of India, this functionality enables users to perform “cardless cash withdrawals” by authenticating transactions through a UPI ID, QR code, or mobile app approval instead of using a physical debit card. The system verifies the transaction in real time, processes the request securely, and allows cash dispensation from linked banking infrastructure or banking agents. This feature enhances financial inclusion, improves accessibility in rural and urban areas, and provides a convenient alternative to traditional ATM-based withdrawals while maintaining strong security and authentication controls.

2. Multi-Bank Connectivity

Multi-Bank Connectivity refers to a feature in digital payment systems that allows a single platform or application to integrate and operate with multiple banks simultaneously. In a UPI-based ecosystem governed by the National Payments Corporation of India, this enables users and merchants to link several bank accounts under one mobile application and seamlessly switch between them for sending or receiving money. It improves flexibility in fund management, reduces dependency on a single banking institution, and allows better control over financial operations. For businesses, multi-bank connectivity supports efficient cash flow distribution, load balancing of transactions, and faster reconciliation across different accounts. Overall, it enhances reliability, scalability, and convenience in digital payment processing.

3. Balance Enquiry System

A Balance Enquiry System is a digital feature that allows users to instantly check the available balance in their bank account or linked payment instrument through a mobile application or payment interface. In a UPI-based ecosystem governed by the National Payments Corporation of India, this system enables users to view real-time account balances securely after authentication using methods like UPI PIN or biometric verification. It eliminates the need to visit a bank branch or ATM for basic balance checks, making financial management more convenient and efficient. The system communicates directly with the user’s bank through secure APIs to fetch accurate and updated balance information. This feature improves transparency, helps users track spending, and supports better financial planning for both individuals and businesses.

4. Mini Statement Support

Mini Statement Support is a digital banking feature that allows users to view a summary of their recent financial transactions in a quick and simplified format. In a UPI-based ecosystem governed by the National Payments Corporation of India, this feature enables users to instantly access a short history of their latest debits and credits directly through a mobile application, ATM, or UPI-enabled interface after secure authentication. The mini statement typically includes details such as transaction date, amount, type of transaction, and remaining balance. It helps users track recent activity without needing to open full account statements, making financial monitoring faster and more convenient. This feature is especially useful for budgeting, fraud detection, and quick verification of payments, improving transparency and user control over banking activity.

5. Instant Transaction Processing

Instant Transaction Processing refers to a real-time payment mechanism that enables financial transactions to be completed immediately between sender and receiver without any delay or batch processing. In a UPI-based ecosystem governed by the National Payments Corporation of India, this process works through a high-speed switching network that connects multiple banks and payment service providers instantly. Once a transaction is initiated and authenticated using secure methods like UPI PIN or biometric verification, the system validates the request, processes the transfer, and sends confirmation to both parties within seconds. This ensures uninterrupted 24/7 fund transfer capability, including weekends and holidays. Instant transaction processing improves cash flow efficiency, reduces dependency on traditional banking hours, and enhances user experience by providing fast, reliable, and seamless digital payments.

Feature Performance Overview

6. Retailer & Distributor Management

Retailer & Distributor Management is a structured system in digital payment platforms that enables the efficient organization, control, and monitoring of multiple business levels such as distributors, retailers, and agents. In a UPI-based ecosystem governed by the National Payments Corporation of India, this system helps platforms manage onboarding, role allocation, commission distribution, and transaction tracking across a large network of partners. Distributors typically oversee a group of retailers, while retailers interact directly with end users to provide services like money transfers, merchant payments, and account support. This structure improves operational efficiency, ensures transparent revenue sharing, supports scalable business expansion, and simplifies administration of large payment networks.

7. Commission Management System

A Commission Management System is a digital feature used in payment and fintech platforms to calculate, track, and distribute earnings or incentives to agents, retailers, distributors, and partners based on their transaction activity. In a UPI-based ecosystem governed by the National Payments Corporation of India, this system automatically applies predefined commission rules for services such as money transfers, merchant payments, bill collections, or onboarding activities. It ensures accurate and real-time calculation of commissions for each successful transaction and maintains a transparent record of earnings across different user roles. The system also supports automated payouts, settlement tracking, and reporting dashboards for better financial visibility. This improves trust, reduces manual errors, and enables efficient revenue sharing across multi-level business networks.

8. Transaction History & Reports

Transaction History & Reports is a feature in digital payment systems that provides users and businesses with a complete record of all financial activities along with structured summaries for analysis and decision-making. In a UPI-based ecosystem governed by the National Payments Corporation of India, transaction history includes detailed information such as transaction ID, date and time, amount, sender and receiver details, and status (successful, pending, or failed). Reports extend this data into organized formats like daily, weekly, or monthly summaries that help businesses track revenue, monitor performance, and reconcile accounts. These reports can often be exported in formats like PDF or Excel for accounting and auditing purposes. This feature improves transparency, simplifies financial management, and supports data-driven decision-making for merchants, distributors, and platform administrators.

9. Analytics Dashboard

An Analytics Dashboard is a centralized reporting interface in a digital payment system that provides real-time insights into transaction activity, revenue performance, and user behavior. In a UPI-based ecosystem governed by the National Payments Corporation of India, it enables merchants, agents, and administrators to monitor key metrics such as total transactions, success and failure rates, settlement status, peak transaction hours, and daily or monthly earnings. The dashboard presents this information through visual elements like charts, graphs, and summary cards, making complex financial data easy to understand and analyze. It helps businesses identify trends, detect anomalies, optimize operations, and make informed strategic decisions. Overall, an analytics dashboard improves transparency, operational efficiency, and data-driven growth in digital payment platforms.

10. Security & Fraud Protection

Security & Fraud Protection in a digital payment system refers to the comprehensive set of technologies, controls, and monitoring mechanisms designed to safeguard users, merchants, and financial institutions from unauthorized access, cyber threats, and fraudulent activities. In a UPI-based ecosystem governed by the National Payments Corporation of India, security is enforced through multiple layers such as two-factor authentication (UPI PIN), encrypted data transmission, secure banking APIs, and device binding to ensure only registered devices can initiate transactions. Features like instant alerts, transaction limits, and risk scoring further strengthen protection. Together, these measures ensure safe, reliable, and trustworthy digital payments while maintaining fast and seamless transaction processing.

System Feature Matrix

| Feature |

Description |

Status |

Priority |

| AEPS Integration |

Aadhaar based cash withdrawal system |

Active |

High |

| Micro ATM |

Card swipe + biometric support |

Active |

High |

| Instant Settlement |

Real-time wallet credit system |

Beta |

High |

| Fraud Detection |

AI-based risk monitoring engine |

Coming |

Medium |

Frequently Asked Questions

A Micro ATM is a portable banking solution that allows customers to access banking

services including withdrawals and balance enquiries through agents or retailers.

Yes. Micro ATM platforms support secure cash withdrawal services through connected

banking networks.

Yes. Retailers and agents can provide banking services and earn commissions using

dedicated modules.

Yes. Modern Micro ATM platforms generally support multiple banking institutions.

Yes. Modern platforms use secure APIs, authentication layers, encryption

technologies, and fraud monitoring systems.

Launch Your Micro ATM Platform

Build a complete Micro ATM ecosystem with cash withdrawals, banking services,

retailer systems, secure APIs, and financial automation.

Request Demo