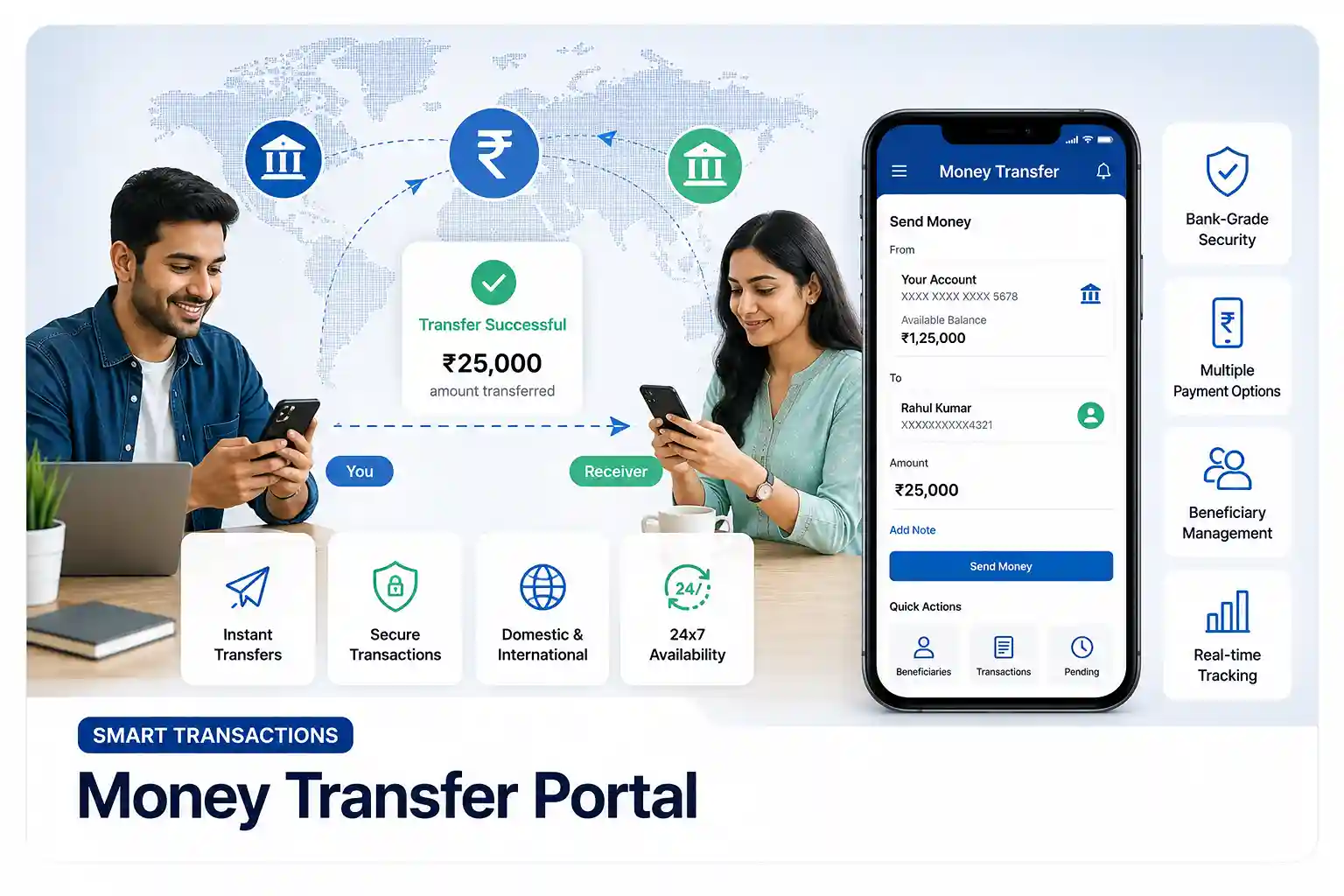

Top Features Every Successful Money Transfer Portal Must Have

The digital payment industry has transformed how individuals and businesses transfer money.

Customers today expect instant, secure, and reliable domestic remittance services that eliminate

lengthy banking procedures and physical visits. Digital money transfer systems allow users to

send funds quickly while maintaining transparency and convenience throughout the transaction

journey.

A modern Domestic Money Transfer (DMT) platform should offer much more than

simple fund transfers. Users expect beneficiary management, instant settlements, transaction

tracking, payment notifications, account history, and secure transaction processing. Businesses

operating financial platforms also require retailer modules, customer dashboards, analytics

systems, and API integrations for scalable growth.

Modern fintech ecosystems frequently integrate services like UPI QR

Payments, BBPS Payment systems, Mobile Recharge platforms, and CRM

solutions. Integrating multiple financial services creates stronger engagement and

improves customer retention.

If you are planning to build a domestic remittance ecosystem, below are the key features every

successful money transfer platform should include.

💳

Sender Pays

➡️

🏦

System Processes

➡️

💰

Receiver Gets Money

1. Domestic Remittance API Integration

API integration serves as the backbone of every money transfer platform. Reliable APIs establish

real-time connectivity with banking systems and payment networks.

This allows users to initiate transactions instantly while reducing processing delays and

transaction failures significantly.

2. Beneficiary Management System

A Beneficiary Management System is a core feature in digital payment platforms that allows users

and businesses to securely add, verify, store, and manage recipients of funds for future

transactions. In a UPI-based ecosystem governed by the National Payments Corporation of India,

beneficiaries can be added using details such as UPI ID, mobile number, or bank account

information. Once a beneficiary is successfully verified, users can make faster payments without

repeatedly entering payment details, reducing errors and improving convenience. The system also

includes security validations like OTP verification and bank confirmation to prevent

unauthorized additions and fraudulent transfers. For businesses, it helps streamline recurring

payouts, vendor payments, and payroll management while maintaining a clear record of all linked

beneficiaries.

3. Instant Fund Transfer Processing

Instant Fund Transfer Processing refers to a real-time payment mechanism that enables money to

be transferred from one bank account to another within seconds, without any delay or batch

settlement cycles. In a UPI-based ecosystem operated by the National Payments Corporation of

India, this process works through a high-speed switch network that connects multiple banks and

payment service providers instantly. Once a transaction is initiated and authenticated using

secure methods like UPI PIN or biometric verification, the system immediately validates the

request, processes the payment, and sends confirmation to both sender and receiver in real time.

This ensures continuous availability of funds transfer services 24/7, including weekends and

holidays. Instant fund transfer processing improves cash flow efficiency, enhances user

experience, and eliminates the delays associated with traditional banking systems.

4. Real-Time Transaction Tracking

Real-Time Transaction Tracking refers to the ability of a digital payment system to monitor and

display the status of a financial transaction instantly from the moment it is initiated until it

is successfully completed or failed. In a UPI-based ecosystem managed by the National Payments

Corporation of India, this feature provides continuous updates on each transaction using a

unique transaction ID, allowing users and merchants to see live status changes such as

initiated, processing, successful, or failed. It ensures transparency by giving instant

visibility into payment flow and helps reduce uncertainty during fund transfers. Businesses can

use this system for reconciliation, reporting, and dispute resolution, while users benefit from

immediate confirmation and tracking through apps or dashboards. Overall, real-time tracking

enhances trust, accuracy, and efficiency in digital payment operations.

5. Multiple Bank Support

Multiple Bank Support refers to a feature in digital payment systems that allows users and

merchants to link and operate more than one bank account within a single platform. In a

UPI-based ecosystem governed by the National Payments Corporation of India, this functionality

enables users to add multiple bank accounts to a single mobile application and choose any of

them for sending or receiving money. It provides flexibility in managing funds, helps separate

personal and business transactions, and improves financial control. Users can also switch

between accounts easily without creating separate profiles or apps. For merchants and

businesses, multiple bank support ensures better cash flow management, load balancing of

transactions, and reduced dependency on a single banking channel, making the payment system more

efficient and reliable.

Transaction Speed Efficiency

Security Strength

User Satisfaction

System Scalability

6. Wallet Integration

Wallet Integration refers to the process of connecting digital wallets with a payment platform

to enable users to store money, make payments, and receive funds seamlessly within a single

system. In a UPI-based ecosystem managed by the National Payments Corporation of India, wallet

integration allows users to link prepaid wallets with UPI applications or merchant systems for

faster and more flexible transactions. It enables instant payments without repeatedly entering

bank details, while also supporting features like balance storage, quick checkout, and

transaction history tracking. For businesses, it improves customer convenience, increases

conversion rates, and supports multiple payment options at checkout. Wallet integration also

enhances user experience by combining banking and wallet functionalities into one unified

digital payment flow.

7. Transaction History & Receipts

Transaction History & Receipts is a feature in digital payment systems that provides users and

merchants with a complete record of all financial transactions along with proof of payment. In a

UPI-based ecosystem governed by the National Payments Corporation of India, transaction history

includes detailed information such as transaction ID, date and time, amount, sender and receiver

details, and current status (successful, pending, or failed). Digital receipts are automatically

generated after each successful transaction and serve as official confirmation of payment. These

receipts can be viewed, downloaded, or shared via SMS, email, or within the application. This

feature improves transparency, simplifies accounting and reconciliation for businesses, and

helps users track and manage their spending efficiently while reducing disputes and manual

record-keeping.

8. Retailer & Distributor Module

A Retailer & Distributor Module is a hierarchical management system used in digital payment

platforms to efficiently manage multiple levels of business users such as distributors,

retailers, and agents. In a UPI-based ecosystem governed by the National Payments Corporation of

India, this module helps platforms onboard, organize, and monitor different partners who

facilitate transactions, merchant onboarding, and payment services. Distributors typically

manage a network of retailers, while retailers directly serve end users or small merchants. The

system includes features like role-based access control, commission management, transaction

tracking, and performance reporting for each level in the hierarchy. This structure improves

operational efficiency, supports scalable business expansion, enables automated revenue sharing,

and ensures better control and transparency across the entire payment distribution network.

9. Analytics Dashboard

An Analytics Dashboard is a centralized reporting tool in a digital payment system that provides

real-time insights into transactions, revenue, and user activity. In a UPI-based ecosystem

managed by the National Payments Corporation of India, it allows merchants, distributors, and

administrators to monitor key metrics such as total transaction volume, success and failure

rates, settlement status, peak usage times, and daily earnings. The dashboard presents this data

in visual formats like graphs, charts, and summaries, making complex financial information easy

to understand. It helps businesses analyze performance trends, identify issues, optimize payment

flows, and make informed decisions. Overall, an analytics dashboard improves transparency,

operational efficiency, and data-driven business growth in digital payment systems.

10. Security & Fraud Protection

Security & Fraud Protection in a digital payment system refers to the set of technologies,

controls, and monitoring mechanisms designed to prevent unauthorized access, fraud, and cyber

threats during financial transactions. In a UPI-based ecosystem governed by the National

Payments Corporation of India, security is ensured through multiple layers such as two-factor

authentication (UPI PIN), encrypted data transmission, secure banking APIs, and device binding

to registered mobile devices. Additionally, real-time fraud detection systems continuously

analyze transaction behavior to identify suspicious patterns and block potentially fraudulent

activities. Features like instant alerts, transaction limits, and risk scoring further enhance

protection for users and merchants. Together, these measures ensure safe, reliable, and

trustworthy digital payments while maintaining fast and seamless transaction processing.

FAST

⚡

Instant Processing

Transfers complete within seconds for better user experience.

SECURE

🛡️

Bank-Level Security

Advanced encryption protects all transactions.

SMART

🧠

Auto Routing

Selects best payment route automatically for faster delivery.

24/7

📞

Always Available

System runs 24/7 without downtime interruptions.

Frequently Asked Questions

Domestic Money Transfer allows users to send money securely within the country

through digital payment systems.

Modern money transfer platforms process transactions instantly or within a short

duration depending on payment networks.

Yes. Beneficiary management systems allow users to add and manage recipient accounts

easily.

Yes. Retailers can process customer transfers and earn commissions using dedicated

modules.

Yes. Modern systems use encryption, fraud monitoring, secure APIs, and OTP

authentication to protect transactions.